Learn the latest trends business innovation with the Educational Programe

Learn the latest trends business innovation with the Educational Programe

Key Definitions:

Satisfaction of one want generates a new want

Wants vary by person, time, and place

Some wants are recurring or complimentary

Wants vary with age, gender, and time

Wants have opportunity costs

Wants are habitual

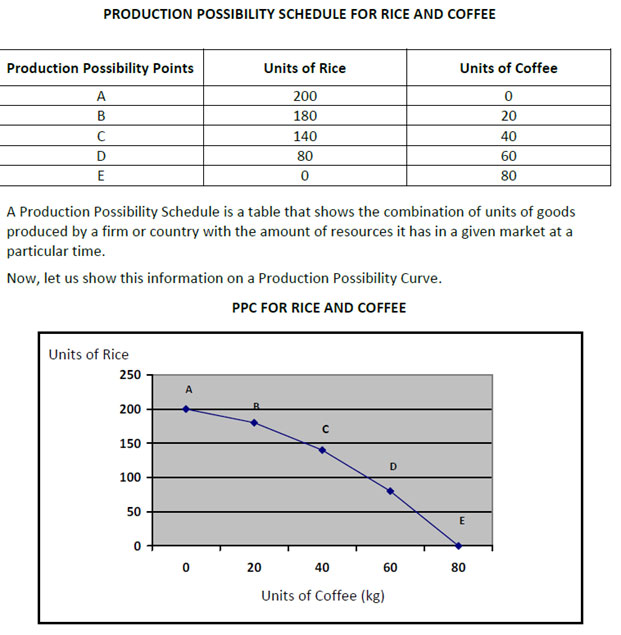

The PPC is an example of an economic model. Economists use economic models to attempt to explain concepts and economic relationships.

In doing this, they make assumptions about parts of the model, thereby simplifying the model.

To move production beyond the frontier, the economy would need to find additional resources to use (increase in labour force or an increase in capital to make workers more productive). Alternatively, a change in technology available might be achieved.

The alternative choices on the PPC e.g., Point A v Point E represent the opportunity costs of choosing different levels of production. By moving from the two points, one sacrifices 200 units of rice and 10 units of coffee for 0 units of rice and 80 units of coffee.

To produce rice at point A, we lose 80 units of coffee, and we gained 200 units of rice. Therefore, 80/200 = 0.4 means that for every 1 unit of rice that is produced, we sacrifice 2.5 units of coffee or 0.4 units of coffee.

Such factors (or their opposites) may shift the PPC to the right (left) and thereby expand (contract) the economy.

There are different types of benefits/costs attached to choices made by individuals, societies, organisations, and countries:

A want is the desire to consume a good/service to get satisfaction or things that we would like to have but are not necessary – we can live without them

Needs are things that we must have to survive, they are necessary

When we make an economic choice/decision we are faced with a cost of making that choice. Therefore, the economic decision that you make to carry out the choice must make full/efficient use of the resources which gives maximum benefit and minimal cost

When a set of resources is used to produce a good/service, alternative goods/services which can be produced with the same set of resources must be give up or scarified. The alternative became the opportunity cost of the choices you have made

The optimum point of production is the point of production where resources are not seen to be under used/wasted

TLP is a Not-For-Profit (NFP) community organisation started and run by volunteers looking to make a difference in the lives of PNG students.